The Indian banking sector has struggled through

a number of rate-setting methods over the last few years and has moved from a benchmark

prime lending rate (BPLR) system to a base rate (or

minimum lending rate) system and now the marginal cost of funds-based lending rate (MCLR).

|

The Reserve Bank of India has brought a

new methodology of setting lending rate by commercial banks under the name

Marginal Cost of Funds based Lending Rate (MCLR). It will replace the existing base rate system

from April 2016 onwards.

According to the new rules, every bank will be

required to calculate its marginal cost of funds across different tenors. To

this, the banks will add other components including operating cost and a tenor

premium.

Why the MCLR reform?

- At present, the banks are slightly

slow to change their interest rate in accordance with repo rate change by

the RBI.

- Commercial banks are significantly

depending upon the RBI’s LAF repo to get short term funds.

- But they are reluctant to change

their individual lending rates and deposit rates with periodic changes in

repo rate.

- Whenever the RBI is changing the

repo rate, it was verbally compelling banks to make changes in their

lending rate.

- The purpose of changing the repo

is realized only if the banks are changing their individual lending and

deposit rates.

|

Implication on monetary policy

- Now,

the novel element of the MCLR system is that it facilitates the so called

monetary transmission. It is mandatory for banks to consider the repo rate

while calculating their MCLR.

- Previously under the base rate system, banks were changing

the base rate, only

occasionally. They waited for long

time or waited for large repo cuts to bring corresponding reduction in

their base rate.

- Now with MCLR, banks are obliged to readjust interest rate

monthly. This means that such quick revision will encourage them to

consider the repo rate changes.

How to calculate MCLR ?

The concept of marginal is important to understand

MCLR.

In economics sense, marginal means the additional or changed situation. While calculating the lending rate, banks have to

consider the changed cost conditions or the marginal cost conditions.

For banks, what are the costs for obtaining funds? It is basically the interest rate given to the

depositors (often referred as cost for the funds). The MCLR norm describes

different components of marginal costs.

A novel factor is the inclusion of interest rate given to

the RBI for getting short term funds – the repo rate in the calculation of

lending rate.

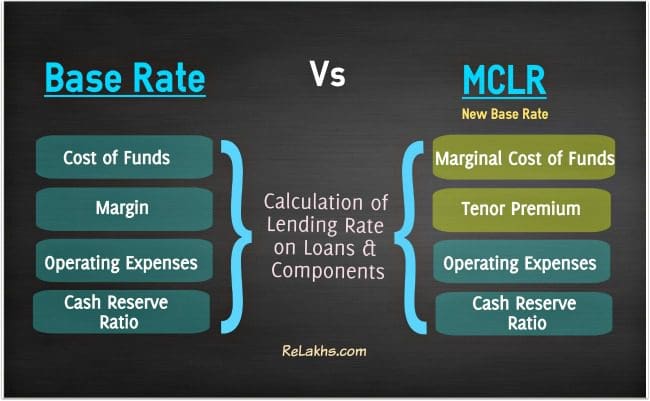

Following are the main components of MCLR.

1.

Marginal cost of

funds;

2.

Negative carry on

account of CRR;

3.

Operating costs;

4.

Tenor premium.

What are these components ?

- Marginal

Cost: The

marginal cost that is the novel element of the MCLR. The marginal cost of

funds will comprise of Marginal cost of borrowings and return on

networth. According to the RBI, the Marginal Cost should be charged

on the basis of following factors:

1. Interest rate given

for various types of deposits- savings, current, term deposit, foreign currency deposit

2. Borrowings – Short

term interest rate or the Repo rate etc., Long term rupee borrowing rate

3.

Return on networth – in accordance with capital adequacy norms.

- Negative

carry on account of CRR: is

the cost that the banks have to incur while keeping reserves with the RBI.

The RBI is not giving an interest for CRR held by the banks. The cost of

such funds kept idle can be charged from loans given to the people.

- Operating cost: is the operating expenses

incurred by the banks

- Tenor

premium: denotes

that higher interest can be charged from long term loans (What is it

exactly ? -->> A tenor premium is the

compensation for the risk associated with lending for a longer time.)

The marginal cost of borrowings shall have a weightage of 92%

of Marginal Cost of Funds while return on networth will have the

balance weightage of 8%.

Moral of the Story being that in essence, the MCLR is determined largely by the marginal

cost for funds and especially by the deposit rate and by the repo rate. Any

change in repo rate brings changes in marginal cost and hence the MCLR should

also be changed.

How MCLR is different from base rate?

So what is common between the two methodologies ?

It is very clear that the CRR costs and operating expenses

are the common factors for both base rate and the MCLR. The factor minimum rate

of return is explicitly excluded under MCLR.

Then whats new in it ?

- The most important

difference is the careful calculation of Marginal costs under MCLR.

- On the other hand

under base rate, the cost is calculated on an average basis by simply

averaging the interest rate incurred for deposits.

- The requirement that

MCLR should be revised monthly makes the MCLR very dynamic compared to the

base rate.

Under MCLR:

1.

Costs that the bank

is incurring to get funds (means deposit) is calculated on a marginal

basis

2.

The marginal costs

include Repo rate; whereas this was not included under the base rate.

3.

Many other interest

rates usually incurred by banks when

mobilizing funds also to be carefully considered by banks when calculating the

costs.

4.

The MCLR should be revised

monthly.

5.

A tenor

premium or higher interest rate for long term loans should be

included.

Advantages ?

- With the inclusion of

shorter term MCLR rates, banks can compete with the commercial paper

market as well.

- moving towards

international standards.

- will reduce the cost

of borrowing for companies.

- will make the lending rate

framework more dynamic as different banks could have different MCLRs for

different tenures.

Demerits / Disadvantages/Roadbloacks/Shortcomings ?

- Banks have been given the option

to keep outstanding loans linked to the base rate system even

though it said existing borrowers will also have the option to move to an

MCLR linked loan “at mutually acceptable terms."

- Most banks are unlikely to offer

this option easily as it means that any immediate hit to profitability may

be avoided.

- Certain loans such as those

extended under government schemes or under restructuring package,

advances to banks’ depositors against their own deposits, loans to banks’

own employees including retired employees and loans linked to a

market-determined external benchmark will be exempt from the MCLR rule.